Blog

The Chat Window Is the New Insurance Agency

Martin, regional insurance executive, begins his morning with a devotional ritual to the old gods: password resets, PDF attachments, and a dashboard that looks like it was designed by a committee trapped in 2014.

He calls this prudence.

His customers call it a reason to procrastinate.

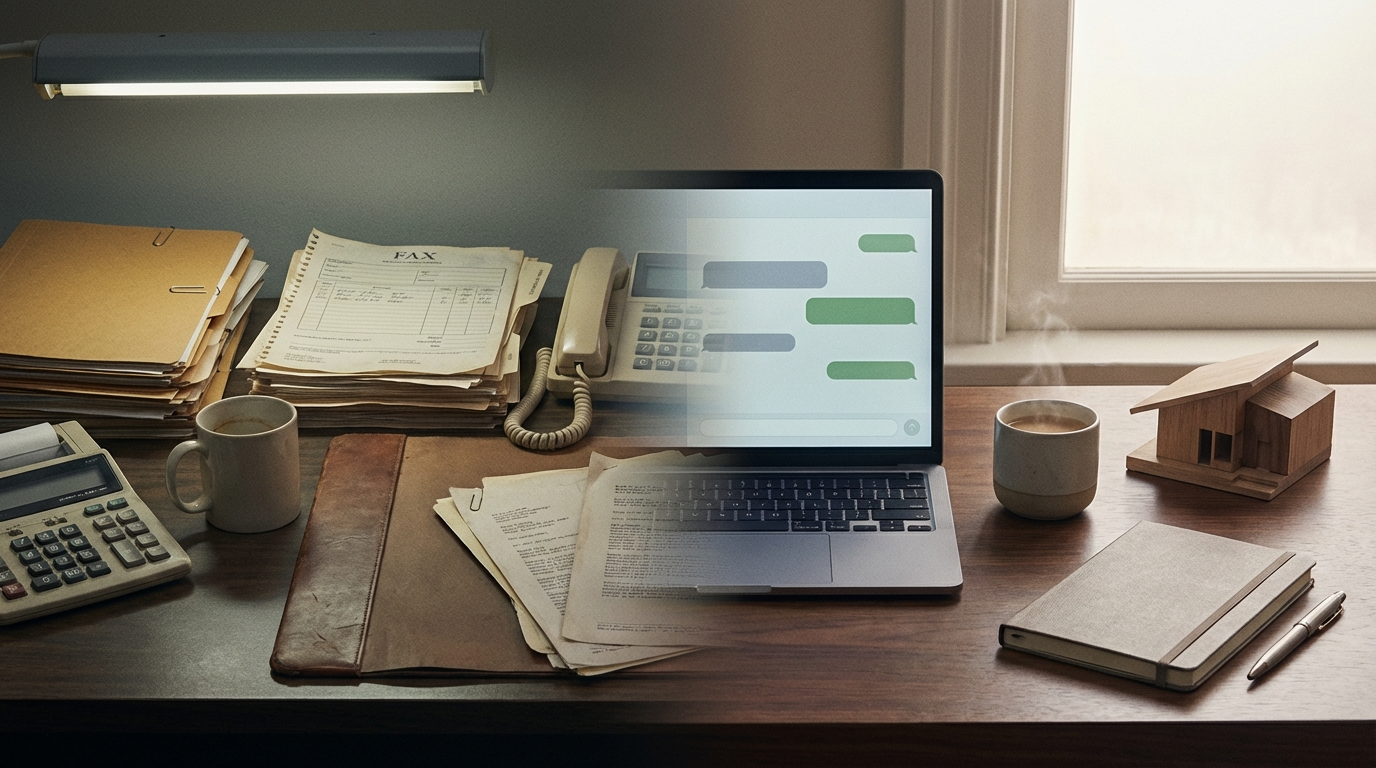

Across town, Lena — landlord, spreadsheet goblin, mild insomniac — is not waiting for a broker callback. She is in a chat window, evaluating a duplex. Rent estimate. Repair assumptions. Insurance cost. Done. One conversation. No swivel-chair theatre. No form that proudly forgets what she entered on the previous screen.

That is not futurism. It is already leaking into the market. This week, Steadily launched a ChatGPT app that lets landlords enter a property address and receive an estimated monthly premium within seconds, as reported by FinTech Global and detailed by ProgramBusiness. The significance is not the gimmick. The significance is the interface.

Insurance distribution has started slipping into the place where people now think.

Not the call center. Not the broker office. Not the sacred portal with eighteen tabs and a soul like damp cardboard.

The chat window.

The Beige Citadel Meets the Conversation Economy

The old insurance stack was built for a world that adored friction because friction looked serious. If a quote required three handoffs, six disclosures, and one tiny act of emotional surrender, surely that meant the process was robust.

What it usually meant was that the customer was doing unpaid integration work for a badly connected company.

AI is tearing up that arrangement. Not because every model is magical. Please. We can retire the incense. It is happening because language is becoming the new operating layer for complex services.

When a customer can ask a system, in plain English, “What would this property cost to insure?” and the system can retrieve relevant facts, call the underwriting engine, interpret the result, and return a usable estimate, the entire value chain starts to compress.

That compression matters.

Distribution gets cheaper. Discovery gets faster. Comparison gets easier. And the carrier that still insists customers should lovingly navigate a maze of brittle forms begins to look less “trusted” and more oddly ceremonial.

The bureaucratic response, naturally, is to squint at the chat box as if it were a raccoon holding a knife.

Useful instinct. Slightly late.

Because once insurance enters an AI-native workflow, it stops being a separate errand. It becomes one ingredient in a live decision loop: buy the property, price the risk, test the cash flow, choose the coverage. The service is no longer visited. It is summoned.

That is a brutal change for incumbents whose moat was mostly made of inconvenience.

The Compliance People Wake Up Sweating

The funniest part of technological history is how often institutions insist something is “just a tool” right up until they need a memo, a task force, and a panel discussion about it.

That phase has begun.

In a recent Insurtech4Good analysis, Andres Lehtmets highlighted that EIOPA Q&A 3407 has been forwarded to the European Commission to ask whether publicly accessible AI chatbots can fall within the scope of insurance distribution under the Insurance Distribution Directive. The practical concern is not theoretical. The cited examples include chatbots suggesting specific insurance products and recommending coverage levels based on personal information and financial constraints.

In other words: the machine may not wear a broker’s shoes, but it may already be doing broker-shaped work.

Good.

That does not mean regulation is obsolete. It means regulation has finally been handed the correct problem.

And yes, there are real risks. Digital Insurance recently laid them out clearly: black-box decisions, embedded bias, weak controls around sensitive data, and AI-enabled fraud from deepfakes to fabricated claims. None of this is imaginary. Insurance runs on trust, documentation, and defensible decisions. If a model cannot explain itself, audit itself, or protect data, it does not belong anywhere near underwriting or claims.

But notice the deeper line in that same piece: the most important risk may soon be not using AI at all.

Exactly.

The old guard wants this debate to sound like courage versus recklessness. It is actually competence versus drift.

There is nothing noble about forcing human staff to spend their lives copy-pasting data between systems because leadership is emotionally attached to a portal.

There is nothing prudent about keeping customers in latency because your architecture cannot answer a question in real time.

And there is certainly nothing “human-centered” about making people beg bureaucracy for clarity when the machine can provide it in seconds.

Underwriting Learns to Speak

The real turn is not that insurance will have chatbots.

The real turn is that underwriting, servicing, fraud detection, and workflow orchestration are starting to converge into one conversational surface.

A recent Digital Insurance commentary on life insurers described what the leaders are doing now: using LLMs to read and interpret policy documents, machine learning to evaluate risk, and agentic systems to execute workflows end to end. That is the important architecture. Language handles intent. Models handle prediction. Agents handle action.

This is how a clumsy institution becomes a responsive one.

Imagine the old claims handler: nineteen browser tabs open, stale coffee, one eye twitching at a scanned PDF named `final_final_v3_reallyfinal.pdf`.

Now imagine the newer stack: first notice of loss arrives, documents are summarized instantly, anomalies are flagged, probable severity is estimated, fraud signals are surfaced, a draft next step is prepared, and the human expert steps in where judgment actually matters.

That is not replacing expertise.

That is rescuing expertise from clerical captivity.

The same pattern will spread across distribution. Customers will not care whether the intelligence lives in a chatbot, an app, a broker co-pilot, or an embedded comparison journey. They will care that the answer is fast, legible, and context-aware.

They will care that the system remembers the conversation.

They will care that insurance finally behaves like software built after the invention of shame.

And once that expectation hardens, the market gets unforgiving very quickly.

No more fictional sketches.

Here is the direct version: insurance is moving from forms to dialogue, from siloed process steps to continuous workflows, from static distribution to intelligent, embedded assistance. The evidence is already visible in live quoting inside ChatGPT, in regulatory scrutiny over whether chatbots are acting like distributors, and in carriers building integrated stacks that combine language models, risk models, and workflow automation.

The winners will not be the loudest AI marketers. They will be the insurers that make their systems explainable, auditable, API-ready, and fast enough to meet customers inside a conversation.

The losers will keep worshipping friction and calling it discipline.

So what exactly are laggards defending? The customer relationship — or the queue? The craft of underwriting — or the inefficiency wrapped around it? If the future customer gets a quote in the same breath as they evaluate a deal, why would they ever come back to the kingdom of hold music, portal passwords, and ceremonial delay?